First-Time Buyer

First-Time Buyer Protocol: Ownership audit vs. Down-Payment Myths

First-Time Buyer Protocol: Ownership audit vs. Down-Payment Myths

The definition of a "First-Time Home Buyer" is simply someone who has not owned a principal residence in the last 3 years.

Even if you owned a home 4 years ago, you now qualify again for first-time buyer grants, down payment assistance, and favorable tax credits.

Require only 3.5% down. This is the classic entry point for buyers with credit scores starting at 580.

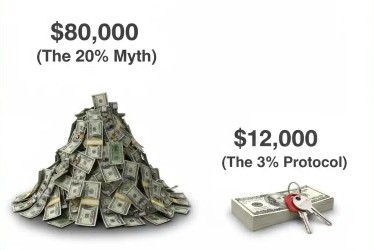

A 3% down option for buyers with higher credit (620+). You don't need $80k to buy a $400k home; you need $12k.

Nevada offers "Home is Possible" grants that can cover up to 5% of your down payment.

Don't just buy a home; buy a roommate layout. Renting out a secondary bedroom can cover 40-50% of your mortgage payment.

You stop paying your landlord's mortgage and start paying your own. Every payment builds equity that you can borrow against later tax-free.